Prospectus Requirements 2026: A Legal Guide for Calgary, San Francisco, and Global Hub Founders

- jzanglaw

- Apr 10

- 13 min read

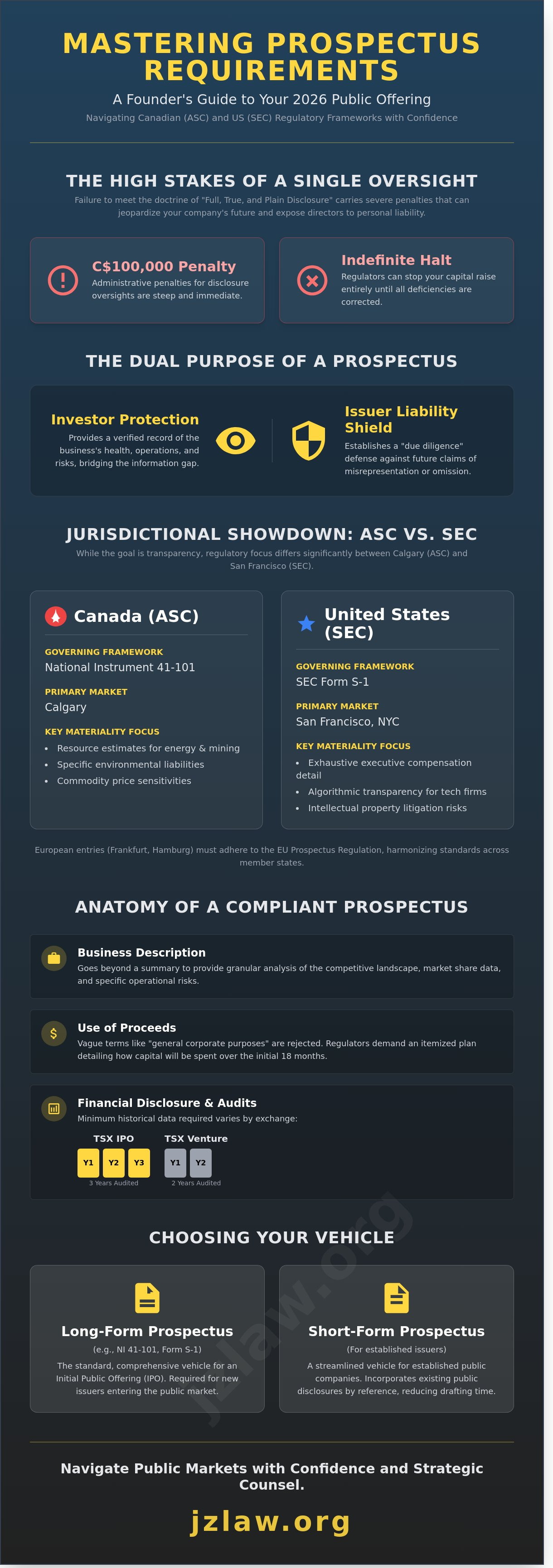

A single oversight in your disclosure documents for a 2026 public offering can trigger a C$100,000 administrative penalty or an indefinite halt of your capital raise. You likely recognize that the regulatory density surrounding the Alberta Securities Commission's latest mandates is becoming increasingly difficult to manage without a strategic partner. The fear of personal liability for even accidental misrepresentation is a valid concern for any founder in Calgary or San Francisco. We understand that your priority is a seamless transition to the public markets without the high costs of non-compliance or the delays of repeated regulatory audits. This guide helps you master the complex legal framework of public offerings by providing a comprehensive breakdown of prospectus requirements across major financial jurisdictions.

Our analysis provides a clear roadmap for your preparation process. We'll examine the critical differences between Canadian National Instrument 41-101 and US SEC requirements to ensure your filing meets the highest standards of precision. By adopting a preventive approach, you can reduce the risk of regulator-mandated revisions and secure your company's financial future with confidence.

Key Takeaways

Understand the fundamental prospectus requirements that serve as both a gatekeeper for public capital and a primary shield against issuer liability in 2026.

Identify the mandatory financial statement thresholds and business disclosure standards necessary to maintain compliance in the Calgary and San Francisco markets.

Evaluate whether a Long-Form or Short-Form prospectus is the optimal vehicle for your specific capital-raising goals and issuer status.

Learn how to implement a robust due diligence defense and structure a professional data room to protect your board of directors during the drafting process.

Leverage strategic cross-border legal counsel to navigate the complexities of simultaneous filings across multiple international jurisdictions.

Table of Contents Understanding Prospectus Requirements: The Gatekeeper of Public Capital Core Components of a Compliant Prospectus in 2026 Comparing Prospectus Types: Choosing the Right Vehicle The Drafting Process: A Step-by-Step Execution Roadmap Strategic Counsel: Navigating Public Markets with JZ Law

Understanding Prospectus Requirements: The Gatekeeper of Public Capital

In the capital markets of 2026, the prospectus remains the definitive legal instrument for any entity seeking to distribute securities to the public. It's the primary disclosure document that bridges the information gap between an issuer and potential investors. Understanding Prospectus Requirements is essential for founders because this document serves a dual purpose. It functions as a mechanism for investor protection while simultaneously acting as a strategic liability shield for the issuing company. By providing a comprehensive, verified record of the business's financial health and operational risks, the issuer establishes a "due diligence" defense against future claims of omission.

Global expansion requires navigating a fragmented regulatory environment. In 2026, the Alberta Securities Commission (ASC) oversees the Calgary market, while the Securities and Exchange Commission (SEC) governs San Francisco's tech-heavy listings. European entries, particularly those in Frankfurt or Hamburg, fall under the scrutiny of BaFin. A critical shift in 2026 is that "plain language" is no longer a stylistic preference; it's a mandatory legal standard. Regulators now routinely reject filings that use dense legalese to obscure risk, demanding clarity that an average retail investor can comprehend without professional assistance.

The Legal Doctrine of Full, True, and Plain Disclosure

This doctrine requires the disclosure of all "material facts." A material fact is any information that would reasonably be expected to have a significant effect on the market price or value of the securities. In Calgary, materiality often hinges on resource estimates or specific environmental liabilities. In New York City or San Francisco, the definition might focus more heavily on algorithmic transparency or intellectual property litigation. Failure to meet these prospectus requirements triggers severe consequences. Under current Canadian law, directors and officers face personal liability for misrepresentations. This means their private assets are at risk if the document contains a misleading statement or a "guilty" omission.

Regulatory Frameworks: NI 41-101 vs. SEC Form S-1

National Instrument 41-101 is the cornerstone of Canadian securities issuance, providing a rigorous template for long-form prospectuses. It's the gold standard for Calgary-based issuers. For San Francisco or Denver startups, the SEC Form S-1 remains the primary vehicle, requiring exhaustive detail on executive compensation and competitive positioning. Founders looking toward European hubs must comply with the EU Prospectus Regulation. This regulation harmonizes standards across Germany and other member states. These frameworks ensure that whether a founder raises C$20 million in Calgary or a larger round in Frankfurt, the level of transparency remains consistent across borders. Our preventive approach ensures that these complex prospectus requirements are met long before the first filing date, protecting the firm's long-term reputation.

Core Components of a Compliant Prospectus in 2026

A compliant prospectus serves as the primary defensive perimeter against future litigation. In 2026, the complexity of prospectus requirements has increased as regulators demand more than just historical data. Founders must present a narrative that balances growth potential with rigorous risk mitigation. Precision here isn't just about compliance; it's about establishing a baseline of transparency that protects the board from future liability.

The business description must go beyond a simple summary of operations. It requires a granular analysis of the competitive landscape and specific market share data. Regulators now scrutinize the "Use of Proceeds" section with unprecedented intensity. Vague descriptions like "general corporate purposes" often result in immediate comment letters. In 2026, the Alberta Securities Commission expects founders to itemize how every C$100,000 will be spent over the initial 18 months. This level of specificity builds investor trust and limits the scope of potential class-action suits based on misallocation of capital.

Financial Disclosure and Audit Standards

For an IPO on the Toronto Stock Exchange (TSX), issuers typically provide three years of audited financial statements. The TSX Venture Exchange usually requires two years. If a Calgary-based firm acquires a competitor representing more than 20% of its consolidated assets, pro-forma financial statements are mandatory to illustrate the combined entity's financial health. Cross-border founders must reconcile IFRS with GAAP, particularly when aligning with U.S. Prospectus Requirements to attract San Francisco venture capital or a dual listing. These prospectus requirements demand a seamless bridge between different accounting philosophies to ensure global investor clarity.

Industry-Specific Disclosure: Cannabis and Crypto

Specific sectors face unique disclosure hurdles. Cannabis companies operating in Alberta or California must disclose regulatory uncertainty, including shifting tax structures and local zoning laws. In the cryptocurrency sector, the focus remains on custody protocols and FINTRAC compliance. As of January 2026, 85% of institutional investors require standardized ESG metrics within the filing. This includes carbon footprint data and board diversity statistics. Strategic planning early in the process ensures long-term stability. Founders often benefit from a preventive legal audit before finalizing their disclosure documents. Every risk factor must be tailored; generic "boilerplate" language is no longer an effective shield in modern securities litigation. Each claim should be backed by a specific date, percentage, or named source to withstand the scrutiny of both regulators and sophisticated investors.

Comparing Prospectus Types: Choosing the Right Vehicle

Selecting the appropriate vehicle for capital raising requires a deep understanding of the regulatory landscape in 2026. The prospectus requirements for a venture depend heavily on the issuer's history and the urgency of the capital need. A long-form prospectus serves as the default requirement for initial public offerings (IPOs), demanding exhaustive disclosure of financial history, management experience, and risk factors. It's the most rigorous path, yet it establishes the necessary transparency for new market entrants in Calgary and San Francisco.

Seasoned issuers often transition to streamlined methods to reduce administrative friction. The short-form prospectus allows companies to incorporate by reference their existing public filings, significantly accelerating the timeline to market. For those seeking maximum flexibility, the shelf prospectus creates a 25-month window during which a company can issue securities without filing a new full document each time. This "shelf" system relies on a base shelf prospectus that outlines the general terms, followed by a supplemental prospectus whenever the issuer decides to "take a draw" from the market. This mechanism is vital for responding to sudden shifts in investor sentiment or commodity prices.

Eligibility for Streamlined Filing

In Canada, eligibility for the short-form system is governed by National Instrument 44-101. To qualify, an issuer must have been a reporting issuer for at least 12 months in a Canadian jurisdiction and be current with all periodic disclosure filings. In the United States, San Francisco founders often look toward Form S-3 eligibility. This requires a public float of at least C$100 million (approximately US$75 million) for primary offerings. Companies with a smaller market capitalization face a heavier regulatory burden, as they cannot easily bypass the comprehensive review cycles associated with long-form filings. Maintaining a clean compliance record is a preventive necessity for any firm planning to utilize these accelerated paths.

The Strategic Use of the Shelf Prospectus

Calgary Energy Sector: Oil and gas firms utilize shelf filings to capitalize on sudden spikes in Western Canadian Select (WCS) prices. Having a shelf ready allows them to secure funding for infrastructure or acquisitions within days rather than months.

San Francisco Tech Hub: High-growth technology companies use "At-the-Market" (ATM) offerings under a shelf prospectus to minimize share dilution. They can sell small increments of stock directly into the market at prevailing prices.

Market Volatility Management: The shelf supplement process enables issuers to pause or accelerate raises based on daily market conditions. This agility is essential in a 2026 economy characterized by rapid interest rate fluctuations.

The cost-benefit analysis of maintaining a current shelf prospectus hinges on the frequency of capital needs. While the initial legal and accounting fees for a base shelf are higher than a single private placement, the per-transaction cost drops significantly over the two-year period. Strategic partners who view prospectus requirements as a tool for market timing rather than just a hurdle often find themselves with a distinct competitive advantage in global financial hubs.

The Drafting Process: A Step-by-Step Execution Roadmap

The transition from a private entity to a reporting issuer requires a disciplined orchestration of legal and financial expertise. It begins with forming a drafting committee comprised of the CEO, CFO, external legal counsel, and lead underwriters. This group's primary objective is to ensure the document satisfies all prospectus requirements while establishing a rigorous due diligence defense for the board of directors.

Under Section 122 of the Securities Act (Alberta), directors face personal liability for material misrepresentations. To mitigate this risk, the committee builds a secure "data room" containing every material contract, board minute, and financial record. This repository serves as the evidentiary basis for the due diligence defense, proving that the company conducted a reasonable investigation into the accuracy of its disclosures before filing. It's a shield that protects the leadership from the fallout of unforeseen market volatility.

Pre-Filing Due Diligence

Verification notes represent the backbone of the drafting phase. For every factual claim or statistic included in the document, counsel requires a source document to verify its accuracy. This process eliminates "puffery" and ensures the 2026 standards for transparency are met. Additionally, the committee must perform "bad actor" background checks on all executive officers and shareholders holding more than 10% of voting rights. For founders in specialized sectors, you can review our guide on taking companies public for additional regulatory context.

Navigating the Review Period

Once the preliminary prospectus, or "Red Herring," is filed on SEDAR+, the regulatory review begins. In 2026, the Alberta Securities Commission (ASC) maintains a standard turnaround time of 10 business days for the first set of comments. Regulators frequently target two specific areas:

Related Party Transactions: Scrutiny of deals between the company and its founders or directors.

Revenue Recognition: Detailed analysis of how the company accounts for long-term contracts or digital assets.

Management must strictly observe "Quiet Period" restrictions during this time. Any public statements that could be seen as promoting the stock can result in the ASC or SEC imposing a "cooling-off" period, which can delay an IPO by 30 to 60 days. After resolving all regulator comments, the company obtains a final receipt and is cleared to launch its roadshow. If you're preparing for a public filing, consult with our securities law team to ensure your documentation survives regulatory scrutiny.

Strategic Counsel: Navigating Public Markets with JZ Law

John Zang provides strategic oversight for complex corporate transactions, ensuring that every filing aligns with the long-term commercial objectives of the issuer. In the 2026 regulatory environment, meeting prospectus requirements involves more than a administrative checklist; it requires a preventive philosophy that identifies potential regulatory friction before it reaches the British Columbia Securities Commission or the SEC. By managing simultaneous filings in Canada and the United States, JZ Law provides a unified legal strategy that eliminates the inefficiencies typical of multi-jurisdictional legal teams.

The firm specializes in high-scrutiny sectors where boilerplate disclosure fails to protect the board of directors. JZ Law applies niche mastery to tailor prospectuses for specific industries:

Oil and Gas: Integrating NI 51-101 reserve reporting with forward-looking financial statements.

Cannabis: Addressing the complex intersection of federal legality and cross-border capital flows.

Crypto and Fintech: Navigating evolving digital asset classifications to ensure compliance with provincial securities acts.

This preventive approach focuses on identifying legal landmines early in the due diligence phase. By resolving issues related to title, intellectual property, or undisclosed liabilities before the preliminary prospectus is filed, the firm reduces the likelihood of costly comment letters and delays from regulators.

Local Expertise in Global Hubs

Founders in Calgary and Alberta's energy sector require legal support that understands the cyclical nature of resource markets. JZ Law provides frameworks for energy-specific listings that balance technical data with investor clarity. You can explore our Oil and Gas Law frameworks for energy-specific listings to see how we handle these complex requirements.

In the San Francisco and Silicon Valley corridor, the firm manages the venture-to-public pipeline. This involves prepping late-stage startups for the transition from private funding rounds to the rigorous prospectus requirements of a public offering on the TSX or NASDAQ. The goal is to maintain the agility of a tech firm while adopting the discipline of a reporting issuer.

The JZ Law Advantage: Efficiency and Precision

Boutique legal counsel often outperforms "Big Law" through superior strategic responsiveness and direct access to senior partners. At JZ Law, clients don't deal with layers of junior associates; they receive direct counsel from John Zang. This model allows for customized tax structuring for public offerings and reverse takeovers (RTOs), ensuring that the transaction is tax-efficient for both the corporation and its shareholders.

Precision in the drafting stage prevents the erosion of shareholder value during the listing process. Whether you're planning an Initial Public Offering or a complex cross-border merger, the firm's focus remains on protecting your reputation and your capital.

Ready to begin your transition to the public markets?Schedule a consultation with John Zang for your 2026 public offering to ensure your legal strategy is as robust as your business model.

Mastering Your Path to Public Capital

Success in the 2026 public markets requires more than just meeting baseline prospectus requirements; it demands a proactive approach to evolving cross-border frameworks. Founders must align the rigorous standards of Canada's NI 41-101 with the specific expectations of the SEC to capture global liquidity. Since the 2023 regulatory shifts in venture disclosures, the margin for error has narrowed significantly. Navigating these complexities without a roadmap often leads to costly delays that can jeopardize a C$20 million raise.

JZ Law provides the strategic foresight needed to bridge the gap between Calgary's resource and tech sectors and the high-intensity markets of San Francisco. Our firm's proven track record includes guiding high-growth ventures through the specialized hurdles of Cannabis and Crypto IPOs. We don't just process paperwork; we build a defensive legal architecture for your firm's long-term stability. By integrating preventive legal strategies early, you ensure your transition to the public eye is both seamless and secure.

Consult with JZ Law on your Prospectus Strategy to secure your position in the global market. Your vision deserves a foundation built on precision and world-class expertise.

Frequently Asked Questions

What is the minimum financial history required for a prospectus in 2026?

Most senior exchanges like the TSX require three years of audited financial statements to satisfy standard prospectus requirements in 2026. Venture issuers or emerging growth companies may qualify for a reduced two-year history if they meet specific market capitalization thresholds. These statements must be prepared according to International Financial Reporting Standards (IFRS) to ensure they meet the expectations of institutional investors in Calgary and San Francisco.

Can a company go public without a full prospectus?

Companies can go public without a full prospectus by utilizing the Capital Pool Company (CPC) program or through a Reverse Takeover (RTO) of an existing reporting issuer. These alternative pathways allow founders to reach the public markets via a filing statement or information circular rather than the traditional long-form document. Statistics from the TSX Venture Exchange show that roughly 50% of new listings choose these alternative routes to manage initial compliance costs and timelines.

How long does the prospectus review process typically take?

The review process for a prospectus generally spans 90 to 120 days from the initial filing date to the issuance of the final receipt. Regulators like the Alberta Securities Commission typically provide their first round of comments within 10 business days of the preliminary filing. The total duration depends on the complexity of the issuer's corporate structure and the speed at which the legal team addresses regulatory queries.

What is the difference between a preliminary and a final prospectus?

A preliminary prospectus is used to market the offering and gauge investor interest, whereas the final prospectus contains the actual offering price and the number of shares sold. The preliminary version doesn't create a legal obligation to sell securities and lacks the final pricing information on the cover page. Once the "book building" process is complete, the final version is filed to legally close the transaction and distribute the shares.

What are the penalties for misrepresentation in a prospectus?

Misrepresentation in a prospectus triggers statutory rights of rescission, allowing investors to cancel their purchase and receive a full refund of their C$ investment. Under the Securities Act (Alberta), directors and officers can face personal liability for damages, and the corporation may be subject to fines reaching C$5,000,000. Our preventive legal strategy emphasizes rigorous due diligence to protect founders from these severe financial and reputational consequences.

Are there specific prospectus requirements for cannabis companies in Alberta?

Cannabis companies must follow enhanced prospectus requirements mandated by CSA Staff Notice 51-352, which focuses on specific disclosure regarding US-based activities and regulatory risks. Issuers are required to provide a detailed breakdown of their licensing status and any potential changes in federal or provincial laws that could impact operations. Since 2018, the Alberta Securities Commission has required these firms to provide quarterly updates on their compliance frameworks to maintain investor transparency.

How do SEC prospectus requirements differ for international issuers?

The SEC allows Canadian issuers to use the Multijurisdictional Disclosure System (MJDS) to satisfy US requirements using their Canadian disclosure documents. This system is a strategic tool for Calgary-based founders because it avoids the need to reconcile financial statements to US GAAP in many instances. International issuers from other regions must typically use Form 20-F or F-1, which involves more intensive regulatory scrutiny than the MJDS pathway.

What is a "Red Herring" and why is it important for the roadshow?

A "Red Herring" is the preliminary prospectus used during the roadshow to solicit non-binding expressions of interest from potential investors. It's the primary tool for communicating the company's value proposition and growth strategy before the final price is determined. The name comes from the red disclaimer printed on the side of the document, which warns that the filing isn't yet final and cannot be used to complete a sale.

Comments