Tax Structuring for High-Growth Companies: 2026 Strategic Legal Guide for Calgary, NYC, and Berlin

- jzanglaw

- Apr 13

- 13 min read

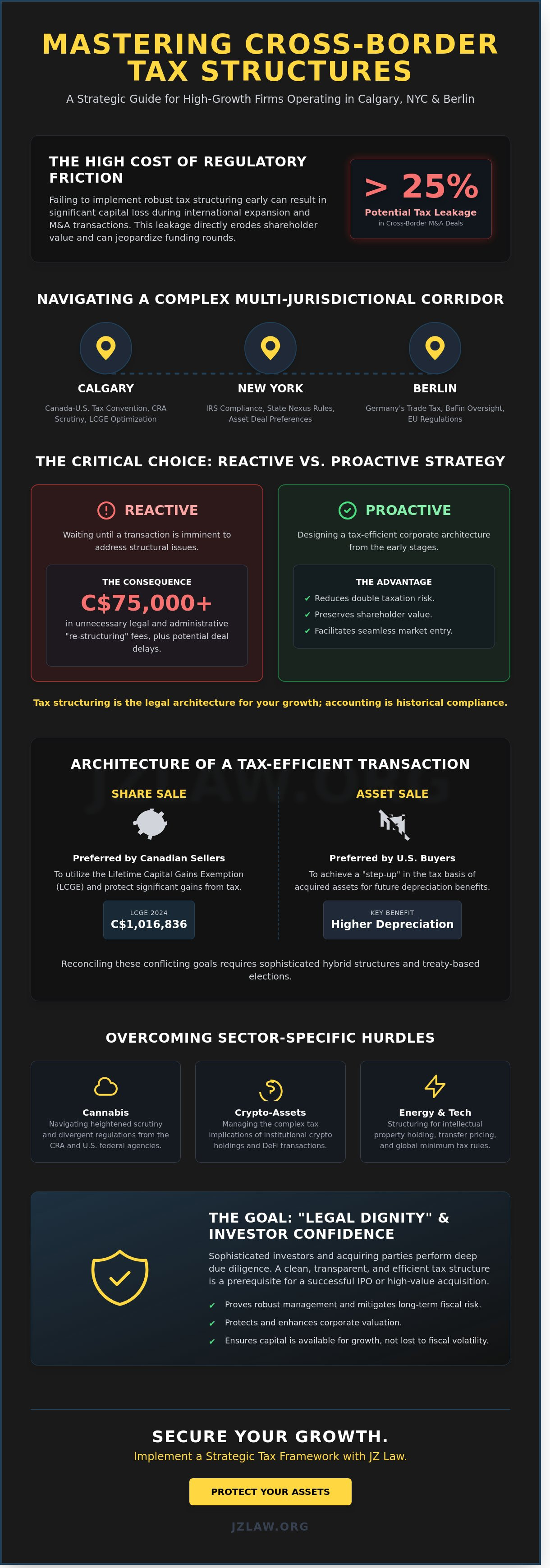

If your firm's valuation scales to C$50 million by 2026, how much of that capital will be lost to regulatory friction across the Calgary, New York, and Berlin corridor? Most founders understand that aggressive expansion often outpaces legal infrastructure, yet failing to implement robust tax structuring early can result in tax leakage exceeding 25% during cross-border M&A transactions. You're right to be concerned about the divergent compliance requirements of the Canada-U.S. Tax Convention versus Germany's trade tax system, especially when sectors like cannabis or crypto face heightened scrutiny from the CRA and BaFin.

This strategic guide will show you how to master the legal frameworks of tax-efficient corporate architecture to protect your assets and optimize transactions in these complex environments. We'll analyze specific jurisdictional risks and provide a roadmap for building a structure that increases shareholder value while ensuring regulatory peace of mind during your next funding round or exit.

Key Takeaways

Learn how to utilize tax structuring as a preventive legal asset to minimize liabilities and ensure total compliance within the complex 2026 regulatory environment.

Identify the strategic advantages of asset-based versus share-based acquisitions to optimize the tax outcomes of your next cross-border M&A transaction.

Overcome sector-specific hurdles, such as the unique tax challenges for cannabis businesses and the complexities of institutional crypto-asset holdings in international hubs.

Master the nuances of the Canada-Germany and Canada-US tax treaties to effectively manage permanent establishment risks when expanding operations from Calgary to Berlin or NYC.

Discover how integrating a personalized legal strategy into your corporate architecture provides a decisive advantage for high-stakes business growth and asset protection.

Table of Contents Understanding Tax Structuring as a Preventive Legal Asset The Architecture of Tax-Efficient Corporate Transactions in 2026 Industry-Specific Structuring: Cannabis, Cryptocurrency, and Energy Sectors Navigating Multi-Jurisdictional Tax Compliance: Calgary to Hamburg Implementing a Strategic Tax Framework with JZ Law

Understanding Tax Structuring as a Preventive Legal Asset

Tax structuring represents the deliberate, legal arrangement of a corporate entity's operations and capital flow to ensure the lowest possible tax liability within the strict confines of global regulatory frameworks. It's a proactive discipline. By understanding tax avoidance strategies, businesses can align their fiscal obligations with their long-term growth objectives. In the 2026 regulatory environment, the distinction between tax planning and tax evasion is sharper than ever. While evasion involves the illegal non-payment or underpayment of taxes through deception, tax structuring utilizes legitimate legal pathways provided by the tax code to optimize a company's financial position.

The division of labor between legal counsel and accountants is critical in this process. Accountants typically focus on historical compliance and the accurate reporting of figures to agencies like the Canada Revenue Agency (CRA) or the IRS. Legal counsel, however, serves as the architect of the corporate structure. We design the legal framework that dictates how those numbers are generated and protected. For high-growth firms in Calgary, Toronto, and NYC, this preventive approach is vital. It addresses the friction between differing provincial and state tax nexus rules before they trigger audits or double taxation issues.

The Strategic Importance of Early-Stage Structuring

Initial entity selection dictates the tax flexibility a startup will have five years down the line. A founder in Vancouver or Denver who chooses a basic incorporation without considering future cross-border expansion often faces "re-structuring" costs that exceed C$75,000 in legal and administrative fees. Pre-structuring avoids this capital drain. It ensures that the transition from a local Canadian CCPC to a multi-state operation in the U.S. doesn't trigger immediate deemed dispositions or exit taxes. Preventive legal oversight manages the complexities of transfer pricing and intellectual property holding long before a transaction occurs.

Reduces the risk of double taxation in international jurisdictions.

Optimizes the C$1,016,836 Lifetime Capital Gains Exemption (LCGE) for Canadian shareholders.

Facilitates seamless entry into the NYC and Berlin markets by aligning with local treaty requirements.

Legal Dignity and Regulatory Compliance

Maintaining a "clean" legal profile is a prerequisite for any firm eyeing an IPO on the Frankfurt Stock Exchange or a major acquisition in New York. Sophisticated investors conduct deep-dive due diligence into a company's tax history. They look for "legal dignity," which is the absence of aggressive, borderline schemes that could invite future litigation or reputational damage. Transparent, tax-efficient structures build investor confidence. They prove that the management team understands the regulatory landscape and has mitigated long-term fiscal risks. Tax structuring serves as a robust shield for corporate valuation by neutralizing fiscal volatility and ensuring that capital remains available for reinvestment rather than being eroded by inefficient legal architecture.

The Architecture of Tax-Efficient Corporate Transactions in 2026

Corporate transactions in 2026 aren't merely about closing deals; they're about long-term tax structuring. High-growth firms operating between Calgary, NYC, and Berlin face a landscape where tax authorities share more data than ever before. Strategic planning must address the 15% global minimum tax rate introduced by the OECD's Pillar Two initiative. While this primarily targets groups with annual revenues exceeding C$1.1 billion, mid-market firms feel the trickle-down effect through increased compliance costs and rigorous reporting requirements to prove their effective tax rate stays above the threshold.

When executing acquisitions, the choice between asset-based and share-based structures remains a primary tension point. In the Canadian market, sellers often insist on share sales to utilize the Lifetime Capital Gains Exemption, which can protect over C$1 million in gains for eligible individuals. Buyers in NYC typically prefer asset deals to achieve a step-up in tax basis for depreciation purposes. Reconciling these conflicting goals requires sophisticated instruments, such as hybrid entities or specific elections under the Canada-US Tax Convention, to ensure neither party inherits unforeseen liabilities.

Effective transaction architecture also relies on holding companies to ring-fence liabilities and optimize flow-through. By utilizing a multi-tiered subsidiary model, a Calgary-based parent company can isolate operational risks in Berlin while maintaining a tax-neutral flow of dividends. If you're looking to protect your domestic assets while expanding, consulting with a strategic legal partner can help clarify these jurisdictional overlaps.

M&A and the Role of Due Diligence

Success depends on a rigorous m&a due diligence process to uncover historical tax exposures that could derail a merger. Parties should use a formal mou to define tax-efficient intent early in the negotiations. For NYC-based operations, referencing official IRS guidance on business structures is vital to ensure the chosen entity qualifies for treaty benefits and avoids double taxation on cross-border distributions.

Financing and Securities Regulation

Choosing between debt and equity financing significantly impacts a firm's tax structuring strategy. Canada's EIFEL rules (Excessive Interest and Financing Expenses Limitation) now restrict interest deductibility to a fixed percentage of tax-EBITDA, making high-leverage strategies less attractive for Calgary firms. NYC and Toronto securities regulators have also tightened oversight on hybrid debt instruments. Companies taking companies public must ensure their pre-IPO restructuring doesn't trigger immediate capital gains, particularly when moving assets between Canadian and US jurisdictions.

Industry-Specific Structuring: Cannabis, Cryptocurrency, and Energy Sectors

Effective tax structuring requires more than a general understanding of corporate law; it demands a surgical approach to industry-specific regulations that vary wildly between Calgary, New York, and Berlin. High-growth firms in the cannabis, digital asset, and energy sectors face disparate fiscal burdens based on their geographic footprint. Precise legal architecture ensures these companies remain compliant while protecting their bottom line from aggressive regulatory shifts.

Cannabis Licensing and Tax-Efficient Operations

Cannabis enterprises operating across the Denver-Vancouver corridor must reconcile vastly different fiscal realities. In the United States, Internal Revenue Code Section 280E continues to prohibit businesses from deducting ordinary business expenses, often resulting in effective tax rates exceeding 70%. Structuring vertically integrated operations requires isolating "cost of goods sold" (COGS) through meticulous accounting to maximize allowable deductions. Conversely, Canadian entities focus on cannabis licensing safeguards during corporate restructuring to prevent the inadvertent triggering of provincial license reviews. Strategic separation of cultivation and retail assets can protect the parent company's valuation during audits; it also facilitates smoother transitions during mergers or acquisitions.

Cryptocurrency and Digital Asset Governance

Institutional crypto-asset holdings in Berlin and New York require distinct governance frameworks to satisfy local authorities. German tax law offers specific advantages for long-term holdings held over one year, whereas New York entities must comply with rigorous SEC and FINTRAC reporting standards to maintain their "qualified custodian" status. The physical and logical segregation of digital assets remains a legal necessity to maintain tax clarity and prevent the commingling of institutional capital with operational reserves. Decentralized Autonomous Organizations (DAOs) now frequently utilize "wrapper" entities in tax-neutral jurisdictions to provide a tax-efficient interface for token-based financing and treasury management. This prevents the entire DAO membership from being treated as a general partnership for tax purposes.

Energy Sector: Calgary and Denver Specialization

In the Alberta energy sector, Calgary-based firms frequently utilize flow-through shares to transfer exploration expenses directly to investors. This mechanism allows companies to renounce Canadian Exploration Expenses (CEE), providing a 100% tax deduction for the investor while the company raises equity capital. Within the framework of oil and gas law, joint venture agreements must be drafted with precision to optimize Capital Cost Allowance (CCA) claims. Establishing environmental reclamation funds as Qualifying Environmental Trusts (QETs) ensures that contributions are tax-deductible in the year they are made. This preserves vital liquidity for future site closures and regulatory compliance. Proper tax structuring in the energy sector often hinges on the timing of these deductions against fluctuating commodity prices.

Preventing audit triggers in these high-regulation fields involves maintaining a clear trail of beneficial ownership and intercompany transactions. Sudden shifts in asset valuation or unexplained cross-border transfers often alert regulators. Proactive legal audits remain the most effective defense against unexpected tax liabilities in 2026.

Navigating Multi-Jurisdictional Tax Compliance: Calgary to Hamburg

Expanding a high-growth enterprise across the Calgary-NYC-Berlin axis requires a sophisticated framework for tax structuring. Companies must reconcile the 1981 Canada-Germany Tax Treaty with the 1980 Canada-US Convention, particularly as the OECD's Pillar Two initiatives reshape global minimum tax standards for 2026. Legal precision in these matters prevents the erosion of capital through double taxation or unforeseen penalties that can arise from inconsistent reporting across borders.

Permanent establishment (PE) risks represent a primary hurdle for New York firms scaling into the German market. A fixed place of business in Berlin, or even a sales representative with concluding authority, can trigger German tax liabilities on global income. To mitigate this, firms often utilize cost-sharing agreements or limited risk distributor models. These strategies ensure that profit allocation remains defensible under audit. Transfer pricing for intellectual property must reflect the arm's length principle; for instance, a C$350,000 annual licensing fee from a Calgary HQ to a Hamburg branch must be backed by a robust 2026 benchmarking study to satisfy both CRA and BZSt requirements.

Dividend Repatriation: Withholding taxes under the Canada-Germany treaty generally drop to 5% for corporate shareholders owning at least 10% of the voting power.

Interest Payments: Structuring debt between a NYC parent and a Calgary subsidiary requires careful navigation of Canada's thin capitalization rules, which limit interest deductibility if the debt-to-equity ratio exceeds 1.5-to-1.

IP Valuation: Professional services firms must document the "DEMPE" functions (Development, Enhancement, Maintenance, Protection, and Exploitation) to justify where value is truly created.

The Germany-Canada Connection: Hamburg and Berlin

German Trade Tax (Gewerbesteuer) is a local levy that varies by municipality, with Berlin's rate currently at 14.35%. Canadian subsidiaries in Frankfurt or Hamburg must balance this with the federal corporate tax of 15.825%. Preventive legal planning is essential for high-net-worth individuals moving between these hubs to avoid "exit tax" triggers that can claim up to 25% of unrealized gains on global assets under Section 6 of the German Foreign Tax Act.

The North American Corridor: NYC, Toronto, and Calgary

The tax disparity between Alberta and New York is stark. Alberta's 8% corporate tax rate offers a competitive advantage for NYC-based venture capital firms looking to invest in Calgary's energy-tech sector. However, cross-listing on the TSX and NASDAQ introduces complex SEC and CSA reporting obligations. Entities must align their tax structuring to manage the 15% US federal withholding tax on dividends while utilizing Foreign Tax Credits (FTCs) to protect their Canadian bottom line and ensure long-term fiscal health.

Secure your international expansion with a strategic legal partner who understands the complexities of cross-border compliance.

Implementing a Strategic Tax Framework with JZ Law

JZ Law treats tax structuring as the skeletal system of a corporation. It isn't a secondary consideration to be handled after a deal closes. Instead, John Zang integrates these fiscal strategies into the very DNA of corporate transactions. This approach ensures that every merger, acquisition, or expansion across the Calgary-NYC-Berlin corridor remains lean and legally defensible. High-growth companies often outpace their initial legal setups within 24 months. JZ Law provides a boutique advantage, offering high-stakes strategy that larger, more rigid firms often struggle to deliver with the same level of personal precision.

The shift from reactive filing to proactive corporate architecture is vital for maintaining liquidity. In the Canadian market, where federal and provincial tax interactions can be intricate, relying on a standard template is a recipe for inefficiency. We replace generic solutions with custom-built frameworks that anticipate regulatory shifts. This methodology doesn't just save money; it builds a foundation that's ready for institutional investment or a public listing. By the time 2026 tax regulations take full effect, businesses that haven't modernized their architecture may face C$100,000 or more in unnecessary overhead annually.

A Strategic Partner for Complex Industries

Our firm specializes in sectors where the law is as dynamic as the technology itself. We represent clients in Cannabis, Crypto, and Oil and Gas, industries that face unique scrutiny from the CRA and international regulators. With a footprint extending from Vancouver to Hamburg, we understand the friction points of global trade. We don't work in a vacuum. JZ Law collaborates with your existing accounting teams to provide a unified legal-financial front. This ensures that the legal entities we create are perfectly mirrored in your financial reporting, reducing the risk of discrepancies during an audit cycle.

Securing Your Corporate Future

The long-term value of a tax-efficient structure lies in its ability to adapt. As we look toward 2026, compliance requirements for cross-border entities are becoming more stringent. An initial consultation allows us to dissect your current structure and identify vulnerabilities before they become liabilities. We focus on securing intellectual property and optimizing holding company locations to protect your capital. It's about moving beyond simple compliance and toward a strategy that supports aggressive growth. You should contact JZ Law for a strategic review of your corporate tax structure to verify that your business is positioned for maximum efficiency in the coming years.

Securing Your 2026 Global Growth Strategy

The 2026 fiscal landscape demands a shift from reactive accounting to proactive legal architecture. For high-growth companies operating between Calgary, NYC, and Berlin, tax structuring serves as a critical preventive asset that safeguards capital during complex cross-border expansions. Navigating the Canadian EIFEL rules or the evolving regulatory frameworks for cannabis and cryptocurrency requires a partner who understands both the letter of the law and the nuances of international trade.

JZ Law brings specialized expertise to the energy and technology sectors, ensuring your corporate transactions withstand the scrutiny of multiple jurisdictions. We don't just solve existing problems; we build frameworks that prevent them. Our team provides strategic legal representation for high-stakes transactions, allowing you to focus on scaling your operations with confidence. It's time to transform your tax obligations into a competitive advantage.

Your firm's resilience depends on the precision of today's decisions. We look forward to guiding your organization through its next phase of global evolution.

Frequently Asked Questions

What is the primary difference between tax structuring and tax planning?

Tax structuring refers to the foundational architecture of your business entities, while tax planning focuses on the annual optimization of financial activities within that established framework. Structuring creates the legal "vessel" across jurisdictions like Calgary and Berlin to minimize long-term liabilities from the outset. It's a proactive, strategic measure taken before significant capital events occur. Planning involves shorter-term adjustments to maximize credits or deductions during a specific 12 month fiscal cycle.

How does tax structuring affect the valuation of my company during an IPO?

Effective tax structuring increases a company's valuation by reducing future tax leakage and ensuring compliance with international regulations like the OECD Pillar Two framework. Investors in 2026 prioritize "clean" balance sheets where deferred tax liabilities are minimized through legal certainty. A robust structure can improve EBITDA margins by 5% to 9%, directly impacting the valuation multiple used by underwriters. Transparent legal frameworks reduce the risk premium that institutional investors apply to high-growth firms.

Can JZ Law help with tax structuring for a cannabis business operating in both Canada and the US?

JZ Law provides specialized legal guidance for cannabis enterprises navigating the conflicting regulatory environments of Canada and the United States. We manage the complexities of the Canadian Excise Act and the US Internal Revenue Code Section 280E, which severely limits business deductions for American operations. Our team ensures that cross-border capital flows don't trigger unnecessary penalties. We've helped firms manage assets exceeding C$25 million while maintaining strict compliance with FINTRAC and US federal guidelines.

What are the risks of ignoring international transfer pricing in 2026?

Ignoring international transfer pricing in 2026 exposes your firm to mandatory 10% penalties on gross adjustments under Section 247 of Canada's Income Tax Act. The global shift toward a 15% minimum tax rate means tax authorities are scrutinizing intercompany transactions more aggressively than in 2023 or 2024. Without documented arm's length pricing, you risk double taxation on profits shifted between Calgary and New York. This lack of compliance frequently leads to multi-year audits that drain corporate liquidity.

Is it possible to restructure a company after a merger has already been initiated?

You can restructure a company after a merger has begun, though it requires complex post-closing integration strategies to rectify tax inefficiencies. Legal teams often utilize Section 85 rollovers in Canada to move assets without triggering immediate capital gains taxes even after the initial deal signatures. It's more cost-effective to align the structure before the 2026 fiscal year begins to avoid retroactive filing fees. Late-stage changes might require court-approved plans of arrangement, which significantly increases your legal expenditures.

How do the tax treaties between Canada, the US, and Germany impact my business structure?

Tax treaties between Canada, the US, and Germany eliminate double taxation by capping withholding taxes on dividends, interest, and royalties at specific rates. For example, the Canada-Germany treaty often reduces withholding on dividends to 5% for qualifying parent corporations. These agreements provide the legal certainty needed for high-growth companies to move capital between Berlin and Calgary. They ensure that profits earned in NYC are recognized fairly when repatriated to a Canadian holding company.

Why should a lawyer, rather than just an accountant, handle my tax structuring?

A lawyer provides solicitor-client privilege, which protects your sensitive tax structuring discussions from being forced into disclosure during a CRA or IRS audit. Accountants are essential for financial compliance and filing, but they don't offer the same level of legal protection or the ability to represent you in tax court. Our firm views the legal structure as the strategic foundation that supports your financial reporting. We ensure that every corporate move is backed by rigorous legal precedent and statutory interpretation.

What specific tax advantages are available for oil and gas companies in Alberta?

Alberta offers the lowest corporate tax rate in Canada at 8%, alongside significant incentives like the Canadian Exploration Expenses (CEE) deduction. Oil and gas companies can often write off 100% of CEE against their income in the year the expense is incurred, providing immediate cash flow benefits. The Alberta Petrochemicals Incentive Program also provides credits for facilities that reach a C$50 million capital investment threshold. These provisions make Calgary a premier hub for energy-sector tax optimization and capital reinvestment.

Comments